The Float:

AI, Corporate Welfare, and Who Holds the Bag

TL;DR

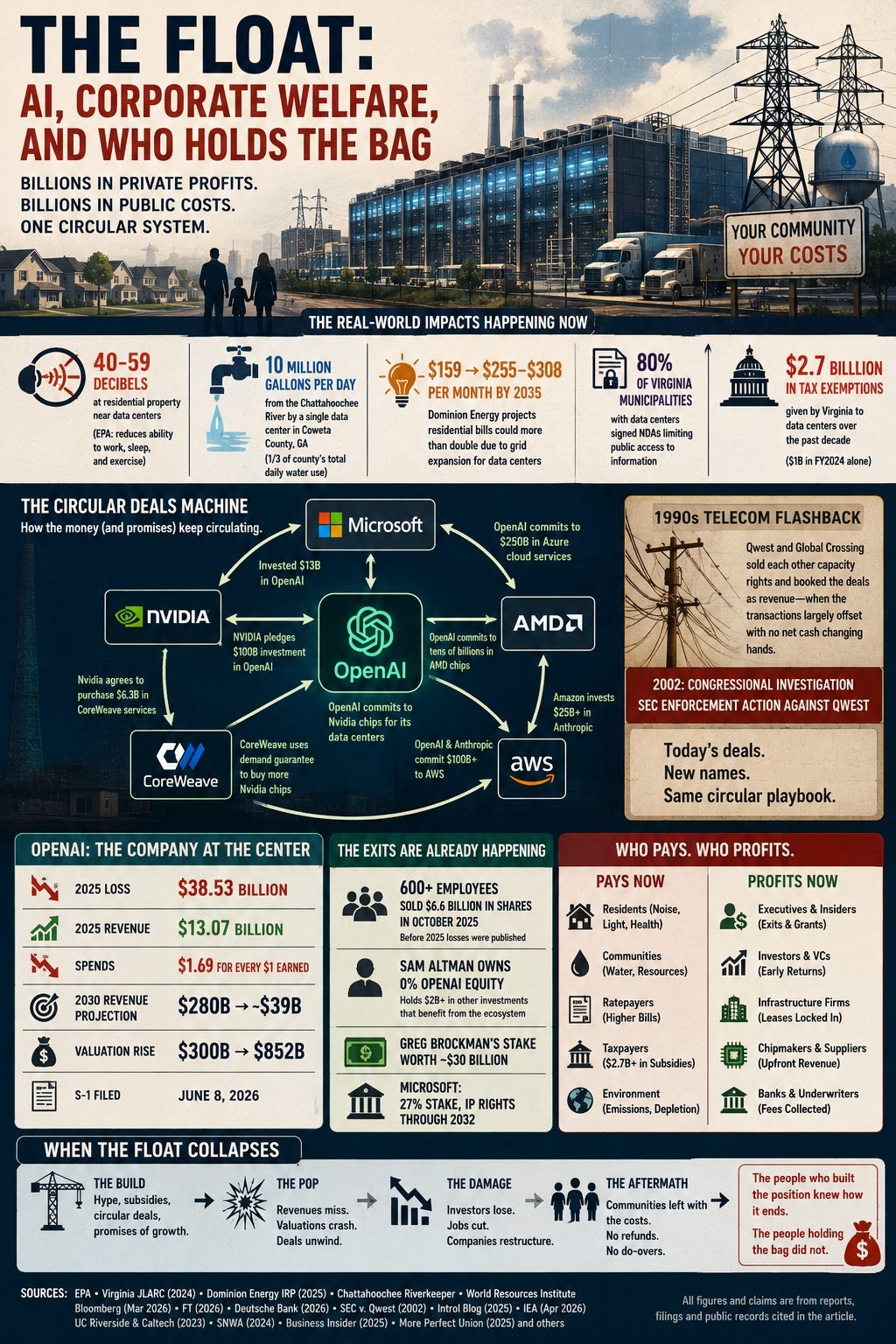

In Chandler, Arizona a quiet residential neighborhood called Brittany Heights sits next to a data center that runs 24 hours a day. Residents describe noise levels that prevent sleep and have made outdoor spaces unusable. In Prince William County, Virginia, nearly one-third of the state’s data centers sit within 200 feet of residentially zoned properties. Residents report chronic noise at levels the EPA says reduce the ability to work, sleep, and exercise. A single data center in Coweta County, Georgia draws nearly ten million gallons daily from the Chattahoochee River, one-third of the county’s entire daily water usage. Virginia residents face utility bills that could more than double by 2035 to pay for grid expansion. Virginia’s governor vetoed a bipartisan bill in May 2025 that would have required studies on noise near homes and schools before approving new facilities. Meanwhile the companies building those facilities are running a circular financial structure that Bloomberg compared to the capacity swap deals that produced a 2002 Congressional investigation and an SEC enforcement action against Qwest Communications. OpenAI lost $38.53 billion in 2025. Its 2030 revenue projection was publicly communicated as $280 billion. The current internal projection is approximately $39 billion. The valuation rose from $300 billion to $852 billion between those two numbers. Over 600 employees sold $6.6 billion in shares in October 2025, before the audited losses were published. The people who built the position are exiting. The people who cannot sleep in Chandler are not on the cap table.

What follows is what the utility commission orders, community impact reports, audited financials, Congressional records, and a 2002 SEC enforcement action say about what is actually happening and who is holding what when it ends.

In 1999 a telecom analyst named Jack Grubman was the most influential voice in the most important sector in the American economy. He covered the companies building the fiber optic network that would carry the internet into the future. He rated most of them as buys. He was employed by Smith Barney, which was collecting hundreds of millions in investment banking fees from the same companies he was rating. When the market collapsed in 2001, Grubman paid a $15 million fine and accepted a lifetime ban from the securities industry. The companies he covered lost a combined $2 trillion in market value. The capacity swaps and vendor financing loops that inflated their revenue were examined by a House subcommittee and pursued by the SEC. The infrastructure built on circular money sat largely unused for years.

None of that stopped anyone from building a functionally similar structure in 2026. It has produced a more sophisticated vocabulary for describing it while it is happening. The word most frequently used is circular. The historical comparison most frequently drawn is to the late 1990s telecom boom.

The question least frequently asked is who is paying for it right now, before the float collapses, while the circular deals are being structured and the S-1 is being prepared.

That question has two answers. One is in the utility commission filings and the community impact reports. The other is in the audited financial statements and the secondary market transaction records. Both answers describe the same machine. They just describe it from different ends.

The People Already Paying

Before the financial structure. Before the float. Before the IPO. People are paying right now.

Brittany Heights is a residential neighborhood in Chandler, Arizona. Residents describe their community as having been transformed after data centers moved in. The noise, a persistent industrial hum from cooling systems that operate continuously, has made outdoor spaces unusable and disrupted sleep for residents who had no advance notice of what was being built adjacent to their homes. This is not an exceptional case. The Environmental and Energy Study Institute documented data center developments in Virginia, Arkansas, Arizona, and Texas illustrating the impact of noise pollution on local residents, with noise levels routinely measured between 40 and 59 decibels on residential property, close to the levels the EPA says reduce the ability to work, sleep, and exercise.

In Northern Virginia, nearly one-third of the state’s data centers sit within 200 feet of residentially zoned properties, per the 2024 Virginia Joint Legislative Audit and Review Commission report. This is possible because zoning ordinances classify data centers as office space rather than industrial facilities. A resident in Prince William County described the experience to Cardinal News: data centers “glow at night like a giant city of lights, humming, pulsating, glowing. The activity never stops.” Residents have complained that the noise prevents sleep and has eliminated their use of outdoor spaces on their own property.

One data center in Coweta County, Georgia draws nearly ten million gallons daily from the Chattahoochee River. That is one-third of the entire county’s daily water usage from a single facility. The Chattahoochee Riverkeeper, which monitors the river running from North Georgia through Atlanta, tracks water usage plans for new facilities in the region. The American Prospect documented that data center developers persuade local leaders of their value by touting construction jobs while the permanent employment is minimal, and that more recent projects are steering away from community benefit agreements entirely.

A review of 31 Virginia municipalities with existing or proposed data centers found that 25, approximately 80%, had signed non-disclosure agreements with developers limiting public access to information about project scale, resource needs, and potential impacts per World Resources Institute research. The residents living next to these facilities frequently were not told what was being built until after the agreements were signed. The impact was a done deal before the public knew to oppose it.

Communities have been pushing back. More than $64 billion in data center projects were delayed or canceled between May 2024 and March 2025 due to organized community opposition, per the Introl Blog analysis. In Indianapolis, Google pulled its $1 billion data center proposal in September 2025 after months of resident opposition. The room filled with people holding signs erupted when the withdrawal was announced. One resident told More Perfect Union: “For a long time it felt like we were four people with cardboard swords fighting a monster. But tonight it shows that people power still rings.”

The political response to this community opposition has been instructive. Virginia Governor Glenn Youngkin vetoed a bipartisan bill in May 2025, HB 1601, that would have required environmental and community impact assessments for proposed data centers, including studies on water use, farmland impact, forest impact, noise near schools and homes, and historic site preservation. The bill was bipartisan. The veto was not. The governor who approved the tax exemptions protecting these companies from competition also vetoed the bill that would have protected the residents living next to their facilities.

In Clayton County, Georgia, the county board of commissioners approved a moratorium on new data centers in 2025. Georgia saw a wave of bipartisan bills in early 2026 responding to what the Georgia Recorder described as “outrage over the surge of data centers.” xAI removed gas turbines from its Colossus data center in Memphis after facing local backlash. Amazon was required to address its acoustical impact after noise complaints in Northern Virginia.

Two business school professors published research in November 2025 finding “no clear evidence that data centers stimulate local growth in tech employment.” The jobs promised during the approval process did not materialize in the communities that accepted the noise, the water consumption, the utility rate increases, and the light pollution.

The people in these communities are not hypothetical future victims of a potential financial unwinding. They are current residents of Chandler and Prince William County and Coweta County who cannot sleep, whose water supply is being drawn down, whose utility bills increased in January 2026, whose governor vetoed the bill that would have protected them, and whose municipalities signed NDAs preventing them from knowing what was coming.

What the Public Is Funding

The community harm is not separable from the public financial subsidy. They are the same transaction viewed from different sides.

Virginia has handed the companies building these facilities $2.7 billion in sales tax exemptions over the past decade. $1 billion in fiscal year 2024 alone, up from $685 million the year before. Virginia’s own Joint Legislative Audit and Review Commission confirmed that exemptions “have grown substantially faster than data center employment.” The IEA documents that a large data center typically employs 25 to 50 direct workers. The community accepted the noise, the water consumption, the light pollution, and the utility rate increases in exchange for tax revenue from facilities that employ approximately 25 to 50 people and receive $1 billion annually in tax relief.

Dominion Energy received approval from the Virginia State Corporation Commission in November 2025 to add $11.24 per month to the average residential bill in 2026, with additional increases projected. Dominion’s own Integrated Resource Plan projects that if data centers do not pay their fair share of grid expansion costs, monthly residential bills could rise from an average of $159 today to between $255 and $308 by 2035. Data center demand contributed to an 833% increase in PJM regional transmission market auction prices for the 2025-2026 period. The 47 gigawatts of contracted demand beyond existing grid capacity is not serving current residents. It is serving the new facilities whose owners received $2.7 billion in tax exemptions while the upgrade costs were distributed to the people already there.

Georgia approved over $1 billion in data center tax exemptions in 2023. Texas is projecting grid strain that ERCOT has flagged as a supply adequacy concern. The deals are made by elected officials. The bills are paid by residents. The community opposition is documented. The NDAs prevented most of those communities from knowing what was coming until after the agreements were signed.

Every major AI company has made public commitments to carbon neutrality or carbon negativity. Then they filed their actual numbers.

Google declared carbon neutrality in 2007. Its 2024 Environmental Report discloses that greenhouse gas emissions increased 48% compared to 2019, with its energy consumption “outpacing” its ability to bring on clean energy. That sentence appeared in a document Google published voluntarily, which raises the question of what the documents they did not publish voluntarily say.

Microsoft pledged to be carbon negative by 2030. In fiscal year 2024 it disclosed emissions had increased 23.4% from its 2020 baseline. The deadline is four years away. The trajectory is moving in the wrong direction at a documented pace. The press releases remain on the website.

Amazon set a net-zero target for 2040 and founded the Climate Pledge, recruiting hundreds of other companies to similar timelines. Since then its absolute carbon emissions have tripled, reaching 68.25 million metric tons in 2024. Amazon has not dissolved the Climate Pledge. None of this seems to have produced a meeting.

The IEA’s April 2026 update documents that AI-focused data center electricity consumption grew 50% in 2025 while global electricity demand grew 3%. Natural gas and coal are projected to meet over 40% of additional data center electricity demand through 2030. The Trellis analysis of the five major tech companies concluded their climate targets “appear to have lost their meaning and relevance.”

The Renewable Energy Certificate is the instrument enabling this gap. A company purchases a certificate representing that a unit of renewable energy was generated somewhere on the same grid. The certificate is retired. The reporting reflects renewable energy use. The electrons powering the servers are the same electrons powering everything else on the grid, including the coal and gas plants that were not retired on the timeline the marketing implied. The certificate does not change the electrons. It changes the sentence in the press release. This is, in the technical accounting sense, legal.

The global observed annual average temperature exceeded 1.5 degrees Celsius above pre-industrial levels in 2024, the warmest year on record per Climate Analytics. The IPCC required emissions to peak before 2025. They did not. Cumulative 2020-2025 emissions were approximately 25% above IPCC pathway requirements. The 1.5 degree target is no longer a warning. It is a missed deadline.

Twenty-three Southern Nevada data centers permanently removed 716 million gallons from the Colorado River system in 2024 per the Southern Nevada Water Authority. Google’s Henderson campus alone accounted for 352 million gallons. Western Resource Advocates estimated in July 2025 that data centers across five Western states could use 7 billion gallons annually by 2035. The federal government paid $28.6 million in 2024 for 110 conservation projects saving 63,631 acre-feet across the Colorado River Basin. The projected data center demand erases those conservation gains entirely. When Business Insider sought water usage records in Western states, utilities blocked the requests or localities redacted data citing commercial trade secrets. The resource is public. The consumption data is proprietary.

Diesel-fueled backup generators at data centers emit 200 to 600 times more nitrogen oxides than natural gas plants when they run, per World Resources Institute analysis, linked to respiratory disease, heart disease, and asthma in surrounding communities. Air pollution from data centers contributed to $1.5 billion in healthcare costs in 2023, a 20% increase from the prior year, per UC Riverside and Caltech research. These costs appear in no technology company’s sustainability report. They appear in emergency rooms and in the lungs of people living in Chandler and Prince William County and Coweta County.The Plagiarism Double Standard

The professor delivering the AI plagiarism lecture deserves a moment of scrutiny before we all nod along.

The textbook they assigned was written by an academic who received a modest advance, reviewed by colleagues who received nothing, published by a company charging $280 for the result, and will be replaced by a new edition in three years to destroy the resale market for this one. The PowerPoint they presented was either their own synthesis of sources they cited but did not create, or the publisher’s instructor resource downloaded from a password-protected website, or some combination of both. The YouTube video they linked in the LMS was produced by someone who received no compensation for its use in a course charging students $3,000 to enroll.

The AI the student used to write the discussion post was trained on every book that professor assigned, every paper that professor published, every lecture that professor recorded and uploaded. Without permission. Without payment. By companies now being sued in federal court by authors including John Grisham, George R.R. Martin, and the New York Times. The Authors Guild filed suit against OpenAI on behalf of authors whose work was ingested without consent or compensation. Meta trained its LLaMA models on LibGen, a piracy database containing more than 7.5 million books, documented in reporting by The Atlantic and confirmed in subsequent litigation. A federal judge, dismissing one case while describing the “historically unprecedented pirating” involved, wrote language approximately as damning as a federal dismissal can be while still being a dismissal.

The student who submitted AI-generated work got expelled.

The companies that ingested the entire written output of human civilization got congressional hearings where they explained fair use to senators who appeared to be encountering the concept for the first time. With patience. And venture-backed confidence.

None of this makes submitting AI-generated work as your own without disclosure appropriate. It makes the institution’s selective enforcement of an intellectual property standard it does not itself meet, while embedded in a publishing system that monetizes publicly funded research without compensating its creators, a monument to the kind of hypocrisy that requires a very large building and a very small mirror.

The Float

The people paying these costs are financing an industry whose financial structure has drawn explicit comparisons to the deals that produced a 2002 Congressional investigation and an SEC enforcement action. That connection is documented and specific, not rhetorical.

In March 2026 Bloomberg published an investigation titled “AI Circular Deals: How Microsoft, OpenAI and Nvidia Keep Paying Each Other.” The structure it documented works as follows.

Microsoft invested $13 billion in OpenAI and secured exclusive Azure cloud rights. OpenAI committed to purchase $250 billion in cloud services from Microsoft. OpenAI committed to purchase tens of billions in AMD chips, with OpenAI becoming one of AMD’s largest shareholders. Nvidia pledged to invest $100 billion in OpenAI. OpenAI committed to stock its data centers with Nvidia chips. Amazon committed $25 billion more to Anthropic. Anthropic committed to spend over $100 billion on AWS over ten years.

The pattern: A invests in B. B uses that capital to purchase A’s products. A books that purchase as projected revenue. A’s projected revenue supports A’s valuation. A’s valuation supports the credibility of its investment in B. B’s receipt of that investment supports B’s valuation. B’s valuation supports the credibility of its purchase commitment to A. The loop closes. Both parties’ financial statements look healthier than the underlying economics alone would justify.

Bloomberg compared this to the capacity swap deals of the 1990s telecom boom. Qwest and Global Crossing sold each other rights to fiber capacity and recorded the transactions as revenue when the deals largely offset each other with no net cash changing hands. The U.S. House Energy and Commerce Subcommittee held hearings in 2002 titled “Capacity Swaps by Global Crossing and Qwest: Sham Transactions Designed to Boost Revenues?” The SEC sued Qwest for securities fraud. Qwest settled for $250 million and restated its revenue.

The Nvidia-CoreWeave arrangement is the most explicit current version of this structure. Nvidia agreed to purchase $6.3 billion in cloud services from CoreWeave. CoreWeave used the guaranteed demand to purchase more Nvidia chips. Those chips were used as collateral for the loans funding the purchase. CoreWeave’s debt received an A3 rating from Moody’s that depends entirely on Nvidia’s demand guarantee. The 7gc.co analysis described this as “functionally equivalent to vendor financing of the 1990s, where equipment manufacturers financed their own sales to recognize immediate revenue while assuming longer-term credit risk.”

Columbia Business School research analyst Gregory Blotnick identified the cascade: “If Microsoft’s AI monetization disappoints, it could reduce Azure spending, impacting Nvidia’s revenue, which would affect CoreWeave’s valuation, ultimately circling back to OpenAI’s funding capacity.”

That is not speculation. That is the load-bearing structure described in consecutive sentences by a named researcher at a named institution.

UBS, JP Morgan Asset Management, and Goldman Sachs have all published analyses noting that today’s hyperscalers have stronger balance sheets than the 1990s telecom companies and that much of the buildout is funded by real operating cash flow. The Big Four tech companies generated $451 billion in operating cash flow in 2024. This counterargument is real and should not be dismissed. The current structure is more resilient than the telecom boom in those specific ways.

What those analyses do not address is OpenAI, which does not share those balance sheet characteristics and which sits at the center of the largest commitments in the circle.

The Company at the Center

OpenAI lost $5 billion in 2024. It lost $38.53 billion in 2025, nearly eight times the prior year, on revenues of $13.07 billion. It spends $1.69 for every dollar it earns. Deutsche Bank projects $143 billion in cumulative negative free cash flow through 2029. OpenAI’s own internal documents project $74 billion in operating losses in 2028 alone before a pivot to profitability in 2029 or 2030. On June 8, 2026, OpenAI filed a confidential S-1 for an IPO. Its current valuation is approximately $852 billion.

The revenue projection supporting the circular deal commitments and the valuation ascent from $300 billion to $852 billion was publicly communicated as $200 billion to $280 billion by 2030. The Decoder reported that a significant portion of that projected revenue was expected from two products that do not yet exist. AI agents capable of replacing human workers in customer service, software engineering, and research were projected to generate up to $29 billion annually, with some variants priced at $20,000 per month. OpenAI has not finalized how to monetize its 500 million weekly free users. The plan to earn billions from advertising and affiliate links is, as TipRanks noted, “still unproven.”

The current internal projection is approximately $39 billion by 2030 according to Sacra’s analysis published in June 2026 using the most current available data. Less than half the prior public figure. The valuation rose from $300 billion to $852 billion while the internal projection was being revised from $280 billion to $39 billion. The S-1 was filed in the window between those two numbers.

This is the specific parallel the Enron instinct is correctly identifying. Enron booked projected future contract revenue as current earnings against assumptions its own traders privately described as indefensible, then hid the resulting losses in approximately 3,000 purpose-built special purpose entities. The question of whether OpenAI’s projections are knowingly false in that legal sense cannot currently be answered without the internal communications from the period when the higher projections were being circulated to investors. What can be stated is the documented sequence: $280 billion publicly communicated, valuation driven to $852 billion, internal projection revised to $39 billion, S-1 filed.

The current AI circular structure is not proven Enron because OpenAI’s losses are disclosed in audited financials verified by the Financial Times. The circular nature of the deals has been reported openly. The distinction matters because calling it Enron before fraud is proven gives the companies a correct and easy dismissal. What cannot be dismissed is the gap between what was publicly communicated and what the internal documents now show. The SEC’s S-1 review will examine whether that gap constitutes material misrepresentation. If the S-1 accurately represents the $39 billion projection, the loss trajectory, and the circular deal dependencies, public investors who buy at a trillion-dollar valuation anyway are making an informed decision. If it does not, the legal term for the difference is securities fraud.

Meanwhile, the Microsoft-OpenAI collapse has already illustrated what happens when collaborative framing meets financial reality. When OpenAI announced a $50 billion partnership with Amazon routing enterprise workloads through AWS, Microsoft responded with unusual directness. A person close to Microsoft told the Financial Times: “We know our contract. We will sue them if they breach it.” On April 27, 2026 the companies announced an amended partnership: Microsoft’s license became non-exclusive, it stopped paying OpenAI a revenue share, and retained a 27% stake valued at approximately $135 billion with IP rights through 2032. The collaboration ended. The financial positions clarified.

Who Walks Away

The exit sequence is already partially complete. Some people have their money. It is documented and it does not go back.

In October 2025, over 600 current and former OpenAI employees sold $6.6 billion in shares through a company-facilitated tender offer. Approximately 75 individuals hit the maximum allowed sale of $30 million each, averaging $11 million per person across all participants. The Wall Street Journal described this as one of the largest employee stock sales in the history of the technology industry. It occurred before the audited 2025 financials showing $38.53 billion in losses were published in June 2026. The people who knew what the 2025 losses would look like exited before the public knew what they were. Whether those 600 people held material non-public information when they sold is already under congressional review.

Court filings from May 2026 confirm Sam Altman holds no direct OpenAI equity. Zero percent. The CEO of an $852 billion company has no equity in it. What he has instead is a documented portfolio worth over $2 billion: a $1.7 billion stake in Helion Energy, which has a $500 million power purchase contract with OpenAI. A $1.2 billion stake in Reddit. Positions in Stripe, Airbnb, Uber, Instacart, Asana, and DoorDash. He has constructed his wealth in companies that benefit from the AI ecosystem OpenAI is creating, without his personal return depending on OpenAI itself succeeding. If OpenAI files for bankruptcy after a failed IPO, Altman personally holds no OpenAI equity to lose. Celebrity Net Worth noted the prediction circulating among close observers: the board will at some point award Altman a retroactive founders grant tied to the IPO hitting a specific valuation. If that grant arrives before the IPO and he sells at the IPO price, that is the exit. If it does not, the parallel portfolio has already captured the upside.

Greg Brockman admitted in court during the Musk trial that his OpenAI equity stake is worth approximately $30 billion, received as a founding grant in OpenAI’s original nonprofit structure.

Microsoft holds a 27% stake, IP rights through 2032, and the Azure infrastructure built to serve OpenAI’s compute needs. Microsoft’s position survives OpenAI’s potential failure more comfortably than any other party because it retains the infrastructure and the intellectual property regardless of OpenAI’s corporate structure.

The data center REITs, Digital Realty and Equinix, have locked in multi-year leases from the hyperscalers with contractual escalators. Those leases survive the AI hype cycle. Digital Realty’s first quarter 2026 revenue was up 16% year over year. BlackRock described the investment thesis: “Power is the gate to that cash flow.”

The infrastructure supply chain, Nvidia, Broadcom, TSMC, Vertiv, Eaton, and Quanta Computer, has collected real revenue during the buildout regardless of the eventual financial structure’s fate. Jensen Huang and other Nvidia insiders sold stock during the AI capex-driven price surge. Those sales are done.

The financial institutions underwriting the $1.5 trillion in projected tech debt issuance have collected underwriting fees at every step. The fees do not go back.

SoftBank led the February 2026 $110 billion round at a $730 billion pre-money valuation and is on paper up $50 billion. SoftBank needs the IPO to realize those gains. Its history with this type of investment is documented. It was the largest investor in WeWork.

Congressional investigators have opened a review of Altman’s personal investments and potential conflicts of interest, examining whether his portfolio companies’ contracts with OpenAI represent undisclosed conflicts. Elon Musk is separately suing OpenAI for up to $135 billion, alleging that the company’s conversion from nonprofit to for-profit public benefit corporation in October 2025 breached its founding agreement. If the Musk lawsuit succeeds, it would represent the first legal finding that the founding commitments were misrepresented. The collaborative framing is dissolving into a legal structure. Each party is reclaiming their position.

The public market investors who buy OpenAI shares at the IPO will be buying at a valuation reflecting a $280 billion 2030 revenue projection that has been internally revised to $39 billion, from a company losing $38.53 billion annually, at the moment when the people who built the position are ready to exit it.

The residents of Chandler and Prince William County and Coweta County are not on the cap table. They received the noise, the water consumption, the light pollution, the utility rate increases, and the NDAs preventing them from knowing what was coming. They do not receive a founders grant. They do not have an exit.

The Broadband Preview

We do not need to speculate about what happens when private companies build utility-scale public infrastructure, capture the market, and price for dependency. The experiment is complete and operating in every American home.

The internet was built on federal research funding, public right-of-way, and government-backed infrastructure investment. It was captured by regional cable and telecom monopolies facing no meaningful competition in most American markets. As of April 2026, Americans achieve a median fixed broadband speed of 308.63 Mbps, ranking 9th globally per Ookla. The U.S. has the third-highest average monthly broadband costs among OECD countries. On a cost-per-megabit basis it ranks in the bottom third of the OECD. France, which required infrastructure sharing mandates, achieved lower prices in comparable density markets, demonstrating that the cost premium in American urban broadband is a policy outcome rather than a geographic inevitability.

Net neutrality rules prohibiting ISPs from throttling, blocking, or charging for priority access were reinstated by the FCC in April 2024. The U.S. Court of Appeals for the Sixth Circuit struck them down entirely on January 2, 2025. ISPs are now legally permitted to create fast and slow lanes and charge websites for priority access. The 23 million low-income households that lost Affordable Connectivity Program subsidies have no federal broadband assistance. Eight and a half million U.S. locations still lack high-speed access entirely.

This is what the capture of public infrastructure by private monopoly looks like after twenty years. The AI infrastructure buildout is the same experiment at a larger scale, faster timeline, with a circular financial structure the broadband monopolies never needed, externalized environmental costs the broadband buildout never generated at this magnitude, and communities with NDAs preventing them from knowing what is being built next to their homes.

When the Float Collapses

When Enron filed for bankruptcy in December 2001, 25,000 employees lost their jobs. They lost $2 billion in pension savings and $1.2 billion in retirement funds concentrated in company stock they were unable to sell while executives were selling. Arthur Andersen, one of the Big Five accounting firms and a 28,000-employee institution, was indicted, convicted, and dissolved within months. The conviction was later overturned by the Supreme Court, but the business was gone. The Sarbanes-Oxley Act passed in 2002 after the damage was complete. The regulation came after the people who needed protection had already been harmed.

The AI buildout’s unwinding would differ in mechanism, in scale, and in one critical respect that changes the consequences permanently.

For investors, the most probable scenario is a controlled unwinding rather than a cliff. OpenAI’s IPO proceeds at a reduced valuation. Earnings disappoint against the S-1’s projections. The circular commitments are renegotiated. Nvidia misses earnings if the OpenAI deal restructures. CoreWeave’s A3 credit rating, which depends on Nvidia’s demand guarantee, is reviewed. The cascade Blotnick described unfolds as a staircase. Public investors who bought at IPO absorb the financial correction. Pension funds holding positions in the AI infrastructure complex through index funds take the diffuse version of the loss. Retail investors in AI infrastructure ETFs absorb what the early holders already exited. The Arthur Andersen equivalent, the ratings agencies that assigned investment-grade ratings to circular structures and the underwriters of $1.5 trillion in tech debt, faces the same congressional inquiry that Andersen faced in 2002. Regulation eventually addresses circular deal revenue recognition and IPO disclosure standards. It arrives after the damage is realized. It always does.

For the communities living next to these facilities, the financial collapse changes nothing about what they are already experiencing. The noise outside the window in Prince William County does not stop if OpenAI files for bankruptcy. The Coweta County water supply does not refill if the circular deal structure unwinds. The utility rate increases embedded in the capital recovery schedules run to 2066 regardless of whether the facilities driving them are still operating. The grid infrastructure built to serve data center demand is in the rate base for forty years. The families paying the increased bills, particularly those in the bottom income quintiles where energy burden is already crossing the severe threshold, do not receive a refund. The ACEEE defines severe energy burden as spending more than 10% of household income on energy. A household earning $35,000 annually paying $381 per month in utility costs by 2045 per Dominion’s own projection would spend approximately 13% of income on energy, well above that threshold. The math is in the utility commission filing.

For the environment, the consequences are permanent in a way that no prior corporate collapse has produced at this scale. The carbon emitted to power the buildout will remain in the atmosphere for centuries. The 716 million gallons removed from the Colorado River system in 2024 do not return. The aquifer depletion in five Western states does not reverse on any human timeline. A financial collapse would produce the regulatory response that politics has blocked, bringing the SEC’s climate disclosure rules back with Congressional backing and finally giving the REC accounting shell game the scrutiny it deserves. But that response addresses future emissions. The emissions already released are already in the atmosphere. The water already consumed is already gone.

For the people in Chandler and Prince William County and Coweta County and Indianapolis and every other community where this buildout has arrived without adequate notice, adequate oversight, or adequate protection, the financial collapse of the circular deal structure produces one practical change: the data centers stop being built. The existing facilities continue operating until they are decommissioned. The noise, the water consumption, the utility rates, and the light pollution continue until someone with standing to require otherwise uses that standing. The NDAs remain in force. The bipartisan bills continue to be vetoed by governors who approved the tax exemptions. The community opposition continues to fight with what one Indianapolis resident accurately described as cardboard swords against a monster.

The difference is that after a financial collapse, the monster is somewhat smaller. The communities that blocked the buildout in time kept the monster out entirely.

The Asymmetry

The 600 employees who sold $6.6 billion in October 2025 have their money regardless of what the S-1 says.

The resident in Chandler who cannot use her backyard does not get her neighborhood back if the float collapses.

The Virginia ratepayer whose bill doubles by 2035 does not get a refund if the projections miss.

The Colorado River does not get its 716 million gallons back if the circular deal structure unwinds.

The people who will live in a climate shaped in part by the decisions being made in these utility commission filings and sustainability reports in 2026 have no legal standing in any current proceeding, no representation on any board, and no voice in any of the decisions being made on their behalf.

The private gains are contingent on projections. The public costs are not. The exits are organized and documented. The harm is distributed and permanent.

This is the structure that has been built before in different industries at different scales. It always ends the same way for the same people. The float works until it does not. The financial participants know this and have structured their exits accordingly. The communities living inside the infrastructure being built to support the float were not offered the same preparation.

The question is never whether the people who built the position knew what they were building. The question is always whether the people holding the bag when the float collapses were told what they were holding.

Most of them were not. Some of them signed NDAs preventing anyone from telling them.

The Receipts

Primary sources throughout. Company filings where available. Congressional records cited by title and proceeding.

Community impact and opposition Environmental and Energy Study Institute, “Communities Are Raising Noise Pollution Concerns About Data Centers” (March 2026). Documents noise levels 40-59 decibels on residential property, Chandler Arizona, Prince William County Virginia: https://www.eesi.org/articles/view/communities-are-raising-noise-pollution-concernsabout-data-centers

World Resources Institute, “From Energy Use to Air Quality, the Many Ways Data Centers Affect US Communities.” Documents 80% of Virginia municipalities with NDAs, backup generator emissions 200-600 times nitrogen oxide levels of natural gas plants, $64 billion in projects delayed or canceled: https://www.wri.org/insights/us-data-center-growth-impacts

Consumer Reports, “AI Data Centers: Big Tech’s Impact on Electric Bills, Water, and More” (March 2026). Documents Indianapolis Google withdrawal, “cardboard swords” quote, November 2025 research finding no clear evidence of local tech employment growth: https://www.consumerreports.org/data-centers/ai-data-centers-impact-on-electric-bills-water-and-more-a1040338678/

The Conversation, “5 Ways Data Centers Endanger Their Local Communities” (June 2026). Documents Prince William County noise, EPA work/sleep/exercise threshold, rural Virginia light pollution: https://theconversation.com/5-ways-data-centers-endanger-their-local-communities-and-the-country-as-a-whole-282348

Cardinal News, “Data Centers Are Changing the Landscape” (January 2026). Documents “glowing like a giant city of lights” quote: https://cardinalnews.org/2025/03/12/data-centers-are-changing-the-landscape-heres-how-they-may-affect-rural-virginia/

Brookings Institution, “Why Community Benefit Agreements Are Necessary for Data Centers” (January 2026). Documents opposition in Ohio, Georgia, Virginia, Arizona, Indiana: https://www.brookings.edu/articles/why-community-benefit-agreements-are-necessary-for-data-centers/

Georgia and moratorium movement Clayton County moratorium documented in Data Center Opposition opposition movement analysis: https://introl.com/blog/data-center-community-opposition-64-billion-backlash Georgia Recorder, “Outrage Over Surge of Data Centers in Georgia Inspires Wave of Bipartisan Bills” (January 20, 2026): https://georgiarecorder.com/2026/01/20/outrage-over-surge-of-data-centers-in-georgia-inspires-wave-of-bipartisan-bills/

Coweta County water The American Prospect, “Demands for Data Center Moratoriums Surge” (December 2025). Documents 10 million gallon daily draw, one-third of county usage: https://prospect.org/2025/12/22/demands-for-data-center-moratoriums-surge/

Virginia governor veto Data Center Watch, “Briefing 05/08/2025.” Documents Governor Youngkin veto of HB 1601

Virginia JLARC report Virginia Joint Legislative Audit and Review Commission, Data Center Analysis 2024. Documents one-third of data centers within 200 feet of residential zones, exemptions growing faster than employment:

https://jlarc.virginia.gov/

Virginia utility rate increases Virginia State Corporation Commission, Biennial Review Order (November 2025):

https://scc.virginia.gov/

Piedmont Environmental Council, “Data Centers and Virginia’s Electric Grid” (November 2025):

https://www.pecva.org/

Virginia data center tax exemptions GovTech, “Virginia Data Center Tax Incentives Have Nearly Doubled” (November 2025): https://www.govtech.com/policy/virginia-data-center-tax-incentives-have-nearly-doubled

Georgia tax exemptions Georgia Budget and Policy Institute (2023):

https://gbpi.org/

ERCOT grid strain Electric Reliability Council of Texas, Supply Adequacy Report (2024): https://www.ercot.com/gridinfo/resource

PJM auction price increase PJM Interconnection, 2025/2026 Base Residual Auction: https://www.pjm.com/markets-and-operations/rpm

AI data center electricity demand IEA, Energy and AI (2025): https://www.iea.org/reports/energy-and-ai IEA, Key Questions on Energy and AI (April 2026): https://www.iea.org/reports/key-questions-on-energy-and-ai/executive-summary

Google emissions Google 2024 Environmental Report: https://sustainability.google/reports/google-2024-environmental-report/

Microsoft emissions Microsoft FY2024 Environmental Sustainability Report: https://query.prod.cms.rt.microsoft.com/cms/api/am/binary/RW1lMjE

Amazon emissions Amazon 2024 Sustainability Report:

https://sustainability.aboutamazon.com/

Trellis climate analysis Trellis, “Climate Goals at Amazon, Apple, Google, Meta, and Microsoft Have Lost Their Meaning” (June 2025): https://www.trellis.net/article/report-climate-goals-amazon-apple-google-meta-microsoft-have-lost-their-meaning/

Renewable Energy Certificates U.S. EPA, Green Power Partnership: https://www.epa.gov/greenpower/renewable-energy-certificates-recs

1.5 degree Celsius target Climate Analytics, “Latest Science on the 1.5°C Limit” (August 2025): https://climateanalytics.org/publications/latest-science-on-the-1-5-c-limit-of-the-paris-agreement IPCC Sixth Assessment Report, Working Group III (2022): https://www.ipcc.ch/report/ar6/wg3/

Colorado River and Western water Southern Nevada Water Authority, 2024 consumption data (Avanza Energy analysis, May 2026)

Western Resource Advocates, July 2025 report: https://qz.com/data-center-water-use-drought-american-west-051326 Business Insider, blocked data requests: https://www.aol.com/data-centers-deepening-water-crisis-164207344.html

Air pollution and healthcare UC Riverside and Caltech, “Data Center Air Pollution” (2024):

https://pacinst.org/

Circular deal structure Bloomberg, “AI Circular Deals: How Microsoft, OpenAI and Nvidia Keep Paying Each Other” (March 11, 2026): https://www.bloomberg.com/graphics/2026-ai-circular-deals/ Global Finance Magazine, “AI’s Financial Circle Game” (February 2026): https://gfmag.com/technology/the-circle-game/ 7gc.co, “AI Capex and the Telecom Bubble” (December 2025): https://www.7gc.co/insights/ai-capex-and-the-telecom-bubble-a-comparative-analysis

Columbia Business School cascade risk Gregory Blotnick, documented in Global Finance Magazine (February 2026): https://gfmag.com/technology/the-circle-game/

Qwest Congressional investigation and SEC action U.S. House Energy and Commerce Subcommittee, “Capacity Swaps by Global Crossing and Qwest: Sham Transactions Designed to Boost Revenues?” (2002) SEC v. Qwest Communications International Inc., Litigation Release 18936: https://www.sec.gov/litigation/litreleases/lr18936.htm

CoreWeave vendor financing 7gc.co analysis: https://www.7gc.co/insights/ai-capex-and-the-telecom-bubble-a-comparative-analysis

OpenAI financial losses Where’s Your Ed At / Edward Zitron, audited financials verified by Financial Times (June 2026): https://www.wheresyoured.at/exclusive-openai-financials/ Fortune, “OpenAI plans to report stunning annual losses through 2028” (November 2025): https://fortune.com/2025/11/12/openai-cash-burn-rate-annual-losses-2028-profitable-2030-financial-documents/

OpenAI revenue projection revision Sacra, OpenAI revenue and funding analysis (June 2026). Documents revised 2030 revenue target approximately $39 billion: https://sacra.com/c/openai/ The Decoder, “OpenAI reportedly plans to grow revenue from $4 billion to $174 billion by 2030”: https://the-decoder.com/openai-reportedly-plans-to-grow-revenue-from-4-billion-to-174-billion-by-2030/

OpenAI S-1 filing FutureSearch AI, “OpenAI Revenue, Losses, and Profitability in 2026”: https://futuresearch.ai/openai-revenue-forecast/

Microsoft-OpenAI contract dispute Data Center Dynamics (March 31, 2026): https://www.datacenterdynamics.com/en/news/microsoft-considers-legal-action-against-openai-and-amazon-over-50bn-contract-report/ eWeek (April 28, 2026): https://www.eweek.com/news/microsoft-openai-deal-multi-cloud-ai-infrastructure/

OpenAI employee share sales American Bazaar Online (May 11, 2026). 600+ employees, $6.6 billion, October 2025: https://americanbazaaronline.com/2026/05/11/hundreds-of-openai-employees-cash-out-6-6-billion-in-shares-480559/Computing.net (May 11, 2026): https://computing.net/news/stocks/600-openai-staff-cashed-out-6-6-billion-in-historic-pre-ipo-share-sale/

Sam Altman equity and portfolio StartupHub.ai (May 2026). Court filings confirm zero direct OpenAI equity: https://www.startuphub.ai/ai-news/ai-figures/2026/figure-sam-altman-venture-portfolio-breakdown-2026-05-27Celebrity Net Worth: https://www.celebritynetworth.com/articles/billionaire-news/why-does-everyone-except-sam-altman-own-equity-in-openai/

Greg Brockman equity admission CNBC (May 12, 2026). Documents $30 billion stake admitted in court: https://www.cnbc.com/2026/05/11/microsoft-ceo-satya-nadella-musk-altman-trial.html

Data center REIT beneficiaries BlackRock, “The Intersection of Infrastructure and AI”: https://www.blackrock.com/us/financial-professionals/insights/investing-in-ai-infrastructure

Enron collapse documented damages Levin Center for Oversight and Democracy, “Congress and the Enron Scandal”: https://levin-center.org/what-is-oversight/portraits/congress-and-the-enron-scandal/

U.S. broadband speeds and costs Allconnect analysis of Ookla Speedtest data (April 2026): https://www.allconnect.com/blog/us-internet-speeds-globally

Net neutrality struck down 6th Circuit Court of Appeals, Ohio Telecom Association v. FCC (January 2, 2025): https://www.dwt.com/blogs/broadband-advisor/2025/01/6th-circuit-fcc-net-neutrality-order

Energy burden American Council for an Energy-Efficient Economy: https://www.aceee.org/research-report/u1602

TL;DR publishes documented arguments on power and the systems that protect it. No claims without sources. No outrage without evidence. If this piece is worth sharing, it will find its own way.